With Keir Starmer in power, savers must act now to protect their wealth from the new Labour government.

Protecting your money had already become more difficult following the Conservatives slashing tax allowances in April, but further changes could follow soon.

Higher-rate, 40pc, taxpayers are already finding themselves £335 worse off as a result of the tax squeeze on savings and investments, according to estimates by wealth manager Quilter.

Investors could face an even bigger hit if Labour subsequently increases taxes.

The capital gains tax allowance has been brutally halved from £6,000 to £3,000 for this tax year, while the dividend tax allowance dropped from £1,000 to just £500. As a result of the cut, an extra 1.1 million people will have to pay dividend tax as of April 2024, according to figures from HMRC obtained in a Freedom of Information request by stockbroker AJ Bell.

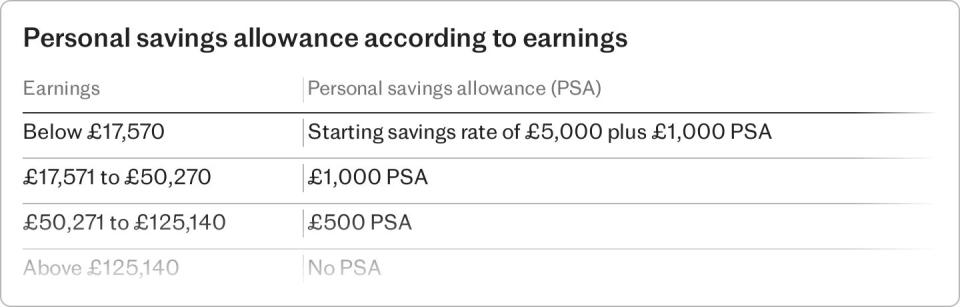

In addition to a tax raid on investment returns, the freeze to the personal savings allowance – the limit to how much savers can earn in interest before having to pay tax – means savers are keeping less of the income they generate from cash.

The personal savings allowance has been frozen at £1,000 for basic-rate taxpayers and £500 for higher-rate taxpayers since 2015. The hundreds of thousands of additional rate taxpayers who entered the 45pc bracket in 2023-24 get no savings allowance.

As savings rates have soared as high as 5pc, a higher-rate taxpayer now needs just £10,000 in savings to exceed their personal savings allowance.

As a result an estimated 2.75 million people paid tax on their cash savings interest in the 2023-24 tax year, according to AJ Bell. This includes around one in 20 basic-rate payers, rising to one in six higher-rate payers and around half of top-rate payers.

The tax raid could be about to get even worse now Labour is in power. The party has been determined to present itself as a tax-cutting party, and repeatedly highlighted former chancellor Jeremy Hunt’s use of “fiscal drag” to raise the tax burden.

The party has ruled out increasing income tax or National Insurance if it wins the next election.

But some believe Chancellor Rachel Reeves will have to raise taxes if the party is to fund its spending pledges – and if that is the case then taxes on “unearned income” from property or share portfolios are an obvious target.

The party has appeared split over capital gains tax – with Angela Rayner, now deputy prime minister and Secretary of State for Levelling Up, Housing and Communities, last year refusing to rule out an increase in the rate during an interview with BBC Radio 4 despite Ms Reeves saying she had “no plans” to do so.

According to analysis by Quilter, an increase to capital gains tax rates under Labour could cost higher taxpayers an extra £900 in tax. This assumes a £250,000 capital gain from a property sale and that capital gains tax rates are aligned with income tax rates, as some have called for.

Selling a second home incurs capital gains tax at 24pc (down slightly from 28pc in 2023-24) if you are a higher-rate taxpayer and 18pc if you pay the basic-rate of income tax. The rate is 20pc and 10pc for other assets such as shares.

The suggestion to align income and capital gains rates was first made by the Office for Tax Simplification, a now-disbanded government agency. If this happened, the capital gains tax rates would be 20pc, 40pc and 45pc depending on the seller’s income tax bracket.

Isas remain the most effective way to shield your savings and investments from any tax changes.

A family of four could stash as much as £116,000 in Isas between now and April 7 2025 using the full allowances available for the 2024-25 and 2025-26 tax years.

Pensions also allow gains to build up free of tax. A family of four, where both parents earn £60,000 each, could add £255,000 over both tax years. Though of course pensions are not accessible until at least the age of 55 and withdrawals are subject to income tax (beyond the 25pc tax-free allowance).

It takes minutes to set up an Isa or self-invested personal pension (Sipp) as long as you have personal and bank account details and National Insurance numbers.

Quilter has estimated that individuals with £20,000 outside of an Isa will lose £135 or £335 this year, depending on their income tax bracket, due to the capital growth being lost to capital gains tax and dividend tax.

Shaun Moore, of Quilter, said: “Lower allowances and higher interest rates mean you will likely find that your personal savings allowance, CGT annual exempt amount and dividend allowance will be decimated very quickly. Even only relatively small gains can waste huge amounts of your allowances next tax year and therefore the sooner assets can be in a tax-sheltered environment like an Isa the better.”

If you currently have investments outside of a tax-free wrapper, you can sell these and move the proceeds into an Isa in a process called “Bed and Isa”.

Over time, the capital gains tax savings can be huge. Assuming a £20,000 investment grows at 7pc a year – with income reinvested – then in ten years’ time you would have a gain worth £19,343, according to Bestinvest. If held in an Isa then all of this would be tax-free – if it is kept outside, then a higher-rate taxpayer would pay £3,269 in tax, assuming the allowance remained at £3,000.

Inheritance tax could be another issue. A leaked recording of a shadow frontbencher has raised fears that the party could be planning a raid on family wealth after death. Darren Jones told a public meeting in March that inheritance tax could be used to “redistribute wealth” and address “intergenerational inequality”. IHT receipts are already at a record high, thanks to frozen tax-free thresholds.

Labour could choose to cut or lower the £325,000 tax-free exemption, widening the scope of inheritance tax, or attack various reliefs that allow people to give away their wealth earlier, without paying death duties. Either move could put your savings at risk, as they’ll form part of your estate when you die.

It may therefore make sense to move money out of your estate. You could do this by making gifts, and using your family’s allowances – this can be helpful for IHT and other taxes, too.

Laura Suter, of AJ Bell, said: “If one half of the couple is a lower earner, or non-earner, there are tax advantages to moving certain investments or savings into their name, to make use of their lower tax rate. At the same time, if one half of the couple hasn’t used up their tax-free allowances in a year and the other has, it might be worth shifting assets to benefit from their personal savings allowance, capital gains tax allowance or dividend tax-free sum.

“Equally if you’ve maxed out your Isa or pension allowances and your spouse hasn’t, you should consider whether you want to move money into their name to use those allowances.”

In addition, you can make use of your children’s allowances. You can invest up to £9,000 into a Junior Isa for your child every year until they turn 18.

As of April 2024 savers can open as many Isas as they want, where previously they could only open one of each type. This will allow savers to more easily take advantage of the top savings rates in the cash Isa market.